More than 20 states now allow pass-through entities (PTEs) to elect to be taxed at the entity level to help their residents avoid the $10,000 limit on federal itemized deductions for state and local taxes, also known as the “SALT cap.” For PTEs electing into a state PTE tax regime, the federal pass-through income of members is reduced by the amount of the state PTE tax, effectively bypassing the member’s state and local tax itemized deduction limitation.

State elective PTE tax regimes generally fall into one of two groups:

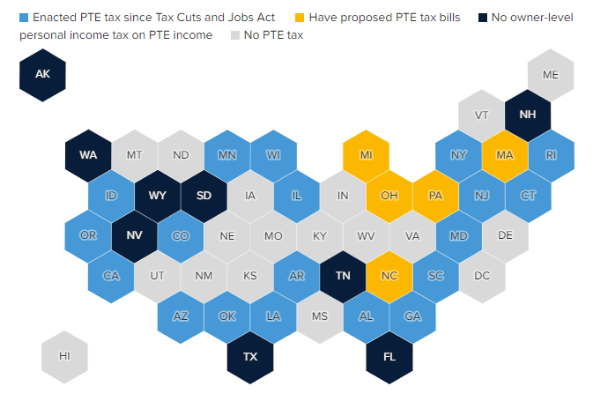

- States in the first group (e.g., Colorado, North Carolina, and Wisconsin) allow members to reduce their adjusted gross income (AGI) by their pro rata or distributive share of income from an electing PTE.

- States in the second group (e.g., California, Illinois, and New York) require members to include their distributive share of PTE income in their AGI but allow members a tax credit for their share of the income taxes paid by the PTE.

State PTE regimes also vary in terms of when and how the PTE tax election must be made, whether the election is binding or can be made annually, who is authorized to make the election on behalf of the PTE and whether members of electing PTEs are required to file returns. Electing PTEs also need to be mindful of whether they are required to comply with a state’s withholding or composite return requirements.

Although the intent behind state PTE tax elections is to benefit the individual members, not all PTE tax elections are advisable. Before making an election, a PTE should model the combined federal and state tax consequences to the PTE — and to each resident and nonresident member — to avoid potential unintended tax results. A robust modeling exercise will include answering the following questions, among others, about the state PTE tax regime and, in some cases, the members’ individual tax situations:

- What is the state’s PTE tax rate, and how is the electing PTE’s tax base calculated?

- Does the state’s PTE tax regime allow net operating losses for the electing PTE or for its members?

- For PTE tax regimes that allow members a credit for taxes paid by the PTE:

- How do members calculate their credit for taxes paid by the PTE, and does the calculation produce a full or partial credit?

- Can non-individual (e.g., corporate) members take a PTE tax credit?

- Is the PTE tax credit refundable or is any excess carried forward?

- Are nonresident members allowed to take an “other state tax credit” on their resident state income tax returns for elective PTE taxes paid to another state?

Insight

When considering a state PTE tax election, one of the most important issues to evaluate is whether members who are nonresidents of the PTE election state may claim a tax credit for their share of the taxes paid by the PTE on their resident state income tax returns. If a state does not offer a tax credit for elective taxes paid by the PTE, then it is possible that a PTE tax election will for some members result in an additional state tax burden that exceeds their federal itemized deduction benefit. Therefore, before making an election, PTEs should consider whether the election would result in members being precluded from claiming other state tax credits — which ordinarily would reduce their state income tax liability dollar for dollar — in order to receive federal tax deductions that are not as valuable.

Tiered Partnerships

Organizations with a tiered partnership structure add an additional layer of complexity to the analysis. Some of the considerations for tiered partnership structures include:

- Does the state’s regime allow a PTE to make the election if it is owned by another PTE?

- When calculating the electing lower tier partnership’s tax base, does it include the income that would flow through to the upper tier partnership?

- Can an upper tier partnership claim a credit or utilize NOLs generated by the lower tier partnership?

Federal Tax Considerations

When deciding whether to make a PTE tax election, taxpayers should not overlook the various federal income tax consequences. For example:

- In what tax year can an electing PTE deduct elective PTE taxes under the federal tax rules? The timing of the PTE’s deduction of the PTE taxes — which determines the timing of the federal deduction benefit for the individual members — will depend on various factors including whether the PTE is on the overall cash or accrual method; whether, in the case of an accrual method PTE, the PTE’s liability to pay the taxes is fixed by the end of the applicable tax year (e.g., when is the PTE election made, or has some overt action taken place by year end to demonstrate an intent to make the election in the subsequent tax year?); and when the tax is paid.

- For example, if an accrual method PTE does not make a state’s voluntary 2021 PTE election and takes no action to demonstrate an intent to make the PTE election by 12/31/2021, the 2021 PTE tax payment that is made by 3/15/2022 would be deductible in 2022, the year the tax is paid, because the liability for the 2021 PTE tax is not fixed by the end of the 2021 tax year.

- Is an owner’s state tax refund attributable to the PTE tax credit considered taxable income for federal income tax purposes, and, if so, to what extent?

- How is the state tax expense of an investment partnership treated? Where the partnership conducts an investment activity and is generating investment income, the PTE tax expense will likely be treated as a Section 212 investment expense subject to applicable limitations on deductibility. Accordingly, the PTE tax election may not reduce the partners’ overall income tax liability.

- Is it possible to specially allocate a partnership’s state tax expense only to those partners whose income was included in the PTE’s state tax base, and, if so, how should the elective PTE state tax expense be specially allocated to comply with the partnership substantial economic effect rules? Note that the partnership or LLC operating agreement may need to be amended to change income and expense allocations.

Financial Statement Considerations

PTEs normally do not provide for income taxes in their audited financial statements as the members are generally responsible for the tax on their share of the PTEs taxable income or loss and would be entitled to any available tax credits on their income tax returns. However, the imposition of a state PTE tax effectively shifts the filing obligation and payment of tax from the members to the PTE, which brings into question whether state income taxes paid by a PTE should be treated as an equity distribution to the members, or as an income tax of the PTE and recorded in accordance with ASC 740. This determination is fact specific and, accordingly, should be made for each jurisdiction in which the PTE pays income tax to conclude whether equity treatment applies, or if the full or partial application of ASC 740 would be more appropriate.

Insight

Regardless of where they operate, PTEs of all sizes should analyze and model the combined federal and state tax effect of a potential state PTE tax election to understand how the election would impact the PTE and each of its members. Modeling should include resident as well as nonresident members and consider the tax consequences of the PTE election on each member’s federal and resident and nonresident state income tax returns.

Feel free to reach out to us to discuss further.